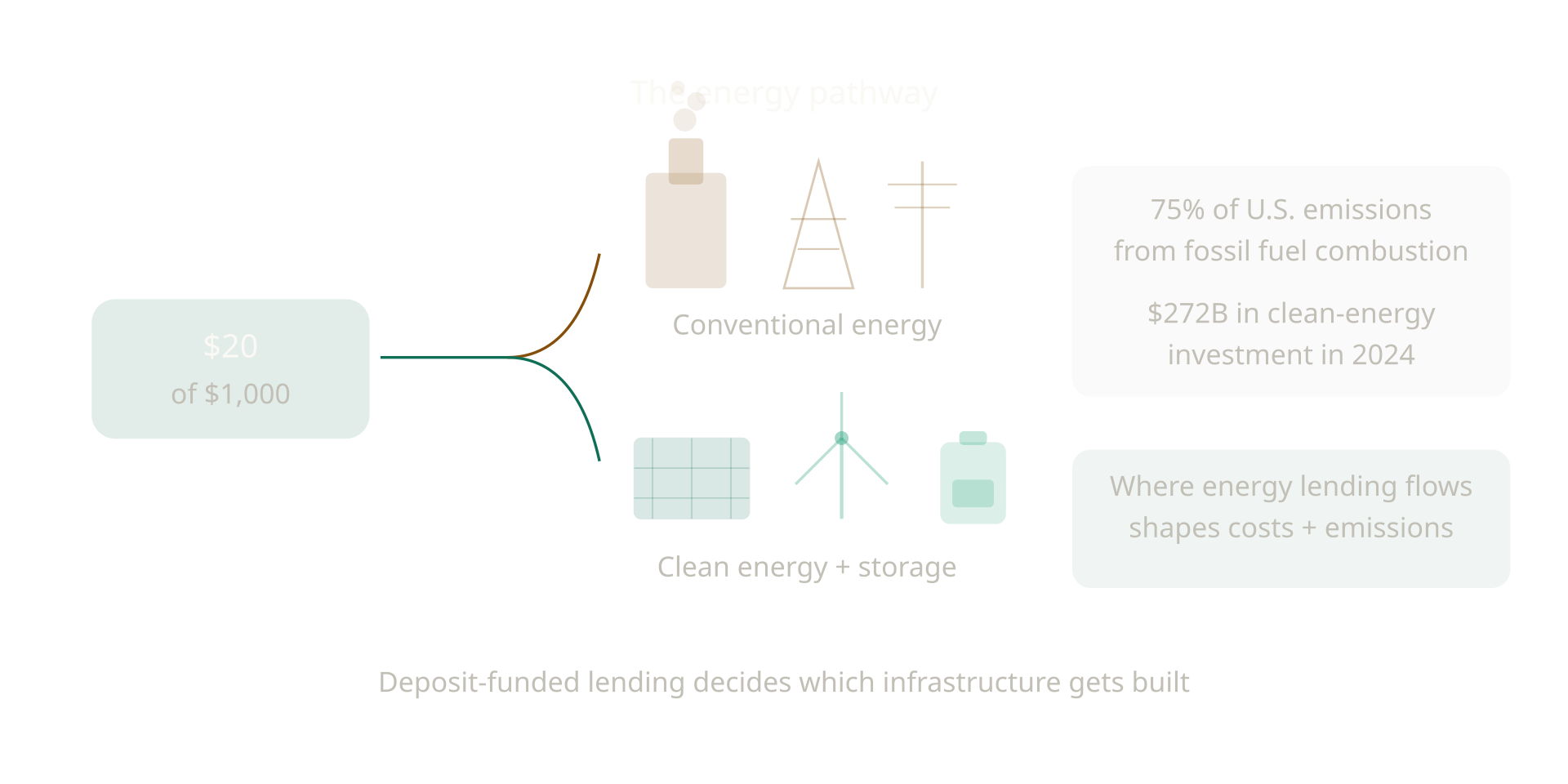

The Energy Pathway – About $20 of Your $1,000

Energy is one of the most capital-intensive parts of the U.S. economy, and therefore a large destination for deposit-funded commercial lending. If you deposit $1,000, roughly $20 of the loaned portion ultimately flows into some part of the energy system including conventional energy infrastructure, regulated utilities, or emerging clean-energy technologies.

Federal Reserve data shows that U.S. banks hold $2.84 trillion in Commercial & Industrial (C&I) loans (5). Although regulators do not publish a granular breakdown of how much of this lending goes to energy borrowers, the best available research indicates that 10–15% of large-bank C&I portfolios are tied to energy-related sectors, including fossil-fuel producers and electric utilities (12). Applied cautiously to the broader system, this implies that $280–$425 billion of outstanding business loans support energy-sector activity.

Bank involvement in the conventional energy system also appears in capital-markets activity. In 2024, U.S. banks participated in $285–$290 billion in fossil-fuel financing (13). Not all of this is deposit-funded lending, but it illustrates how deeply embedded long-lived conventional energy assets remain in financial portfolios.

At the same time, banks are expanding financing for emerging energy technologies. U.S. clean-energy investment reached $272 billion in 2024 (14), and a growing share of that investment is now debt-financed as technologies mature and cash flows stabilize. This includes commercial solar, battery storage, efficient buildings, electrification upgrades, and community-scale energy systems.

Energy lending determines which infrastructure gets built and maintained, with cascading effects on costs, emissions, and community outcomes. Fossil-fuel combustion still accounts for roughly three-quarters of U.S. greenhouse gas emissions, with the power sector contributing about 25% (15). Because banks supply significant capital to this system, deposit-funded lending flows, toward established infrastructure or emerging alternatives, shape energy costs, emissions outcomes, and infrastructure resilience nationwide.

Energy burden: One in four low-income households spends over 15% of income on energy bills, triple the national average, a gap that access to efficiency financing could significantly narrow (16).

Health and economic costs: Air pollution from energy infrastructure contributes to respiratory illness and premature mortality, creating measurable economic burdens through healthcare costs and lost productivity, with impacts concentrated in communities adjacent to older facilities (17).

Technology access: Only 16% of U.S. homes use heat pumps and just 1% use heat-pump water heaters (18), reflecting the upfront capital barriers that limit access to lower-cost, modern heating and cooling systems.

Grid resilience: Underinvestment in grid modernization leads to more frequent and longer outages, particularly in economically vulnerable communities where recovery resources are limited (19). Where grid lending flows determines which neighborhoods gain access to reliable, resilient electricity infrastructure.

Across affordability, grid reliability, air quality, emissions, and access to modern technologies, the flow of deposit-funded lending becomes the flow of opportunity. Even a small share of your $1,000 helps shape the energy systems people depend on every day.